Table of Contents

Multinational corporations operating in Thailand as Foreign Business Entities frequently encounter a significant regulatory obstacle: the inability to distribute dividends despite having sufficient liquidity, due to the presence of "Retained Losses" on their financial statements.

The statutory crux of this limitation is governed by Section 1201, Paragraph Three of the Civil and Commercial Code, which explicitly mandates:

"No dividend shall be declared except out of profits, and no dividend shall be paid as long as the company has a retained loss."

In practice, this implies that even if a corporation achieves substantial current-year net profits (e.g., 100 million THB), the existence of even a nominal retained loss from prior fiscal periods strictly precludes the declaration of dividends until such losses are fully extinguished.

To facilitate the legitimate and compliant repatriation of funds to the Group under such circumstances, Legal Unit recommends the following three strategic frameworks, while advising caution regarding their respective "regulatory traps"

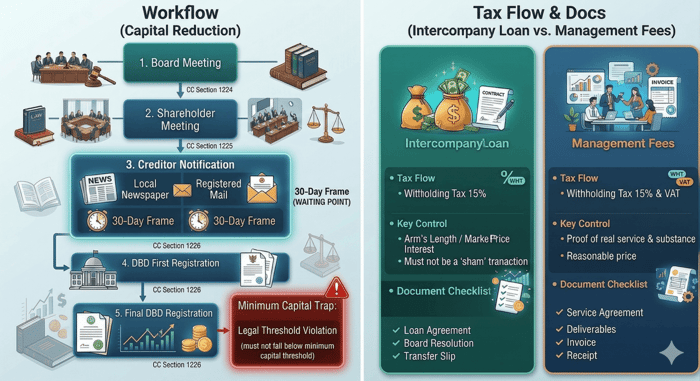

1. Capital Reduction to Offset "Retained Loss"

- The Strategy: For entities seeking to "clear the slate" and restore future dividend capacity, reducing registered capital under Sections 1224 - 1226 of the Civil and Commercial Code is a highly transparent mechanism. The surplus generated from this reduction is utilized to offset accumulated losses or return excess capital to shareholders.

- Statutory Procedure: Due to the impact on creditor confidence, the law mandates a rigorous process:

- Step 1: Board Meeting: To pass a resolution convening a shareholders' meeting. Under Section 1225, capital cannot be reduced below one-fourth (25%) of the total original capital.

- Step 2: Shareholders' Meeting & Special Resolution: Requires approval by at least three-fourths (3/4) of the total votes of shareholders present and entitled to vote.

- Step 3: Creditor Notification: Within 14 days of the resolution, the company must publish a notice in a local newspaper and send registered notification letters to all known creditors.

- Step 4: Waiting Period: Creditors are afforded 30 days to object. The reduction cannot proceed until objecting creditors are satisfied or provided with security.

- Step 5: Registration: Register the special resolution with the Department of Business Development (DBD) within 14 days, followed by the final registration of the capital reduction after the 30-day notice period ends.

- The "Minimum Capital Trap": Entities holding a Foreign Business License (FBL) must ensure capital does not fall below the statutory minimum (e.g., 2 million THB for general business or 3 million THB per category). Furthermore, entities with multiple licenses must maintain sufficient capital for each individual category without overlapping.

2. Transitioning from Dividends to "Intercompany Loans"

- The Strategy: When dividends are restricted despite excess cash, reclassifying the funds as a "receivable" via an Intercompany Loan is a prevalent approach. The Thai subsidiary provides financing to the parent company for Group-wide working capital.

- Legal & Tax Compliance:

- FBA Compliance: Foreign entities must verify if their FBL covers "lending to affiliates" under Category 3 (21). Absence of such authorization may necessitate additional permission or reliance on Ministerial Regulation exemptions.

- Transfer Pricing: Interest must be charged at an "Arm’s Length Price" (Market Rate). Failure to do so empowers the Revenue Department to assess additional income under Section 65 Bis (4) of the Revenue Code.

- Withholding Tax (WHT): Interest remittances are subject to WHT, managed according to Thai law and relevant Double Tax Agreements (DTA).

- Risk Mitigation: The transaction must possess genuine commercial substance and must not be a "sham" designed solely to circumvent dividend restrictions, as this may be characterized as tax evasion.

3. Implementing "Management & Service Fee" Arrangements

- The Strategy: Where the parent company provides legitimate support—such as know-how, IT infrastructure, or strategic consulting—the subsidiary may remit "Service Fees" in lieu of waiting for dividend distribution.

- Compliance Principles:

- Substance over Form: Services must be actually rendered, and the Thai subsidiary must derive a demonstrable benefit. Comprehensive documentation (Deliverables) such as meeting minutes or reports is mandatory to prevent characterization as a "Transfer of Profits".

- Arm’s Length Principle: Fees must align with rates charged to independent third parties and must be justifiable through benchmarking.

- Tax Obligations: Remittances typically incur a 15% Withholding Tax (subject to DTA) and 7% VAT (via P.P. 36).

- Key Advantage: These fees are generally deductible as business expenses, thereby optimizing the Corporate Income Tax base for the Thai entity

💡 Legal Unit’s Insight: Strategic Selection

When "Retained Loss" becomes a legal barrier to dividend distribution, the solution lies in selecting the "Legal Tool" that best suits the company's current status. While Capital Reduction addresses long-term structural issues, Intercompany Loans or Service Fees provide short-term flexibility. Often, a Mix & Match approach provides the highest level of adaptability.

The ultimate priority remains a comprehensive Legal & Tax Health Check to evaluate constraints related to retained losses, license conditions (FBL), and transfer pricing regulations.